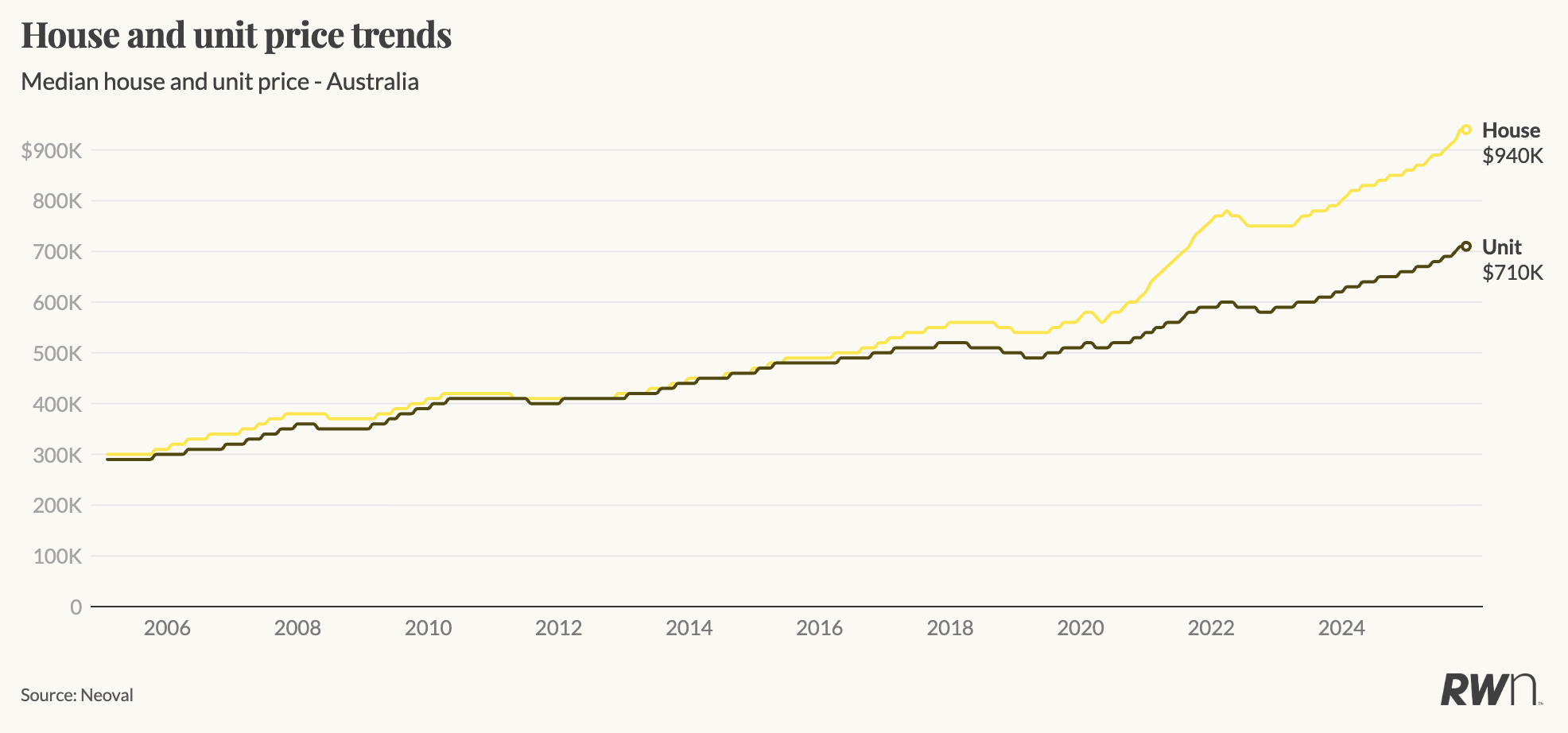

Australia’s housing market levelled out in November, with both national house and unit prices unchanged over the month at $940,000 and $710,000 respectively. This follows steady gains through spring, including the 1.1 per cent rise in October that pushed annual house price growth into double-digit territory sooner than expected.

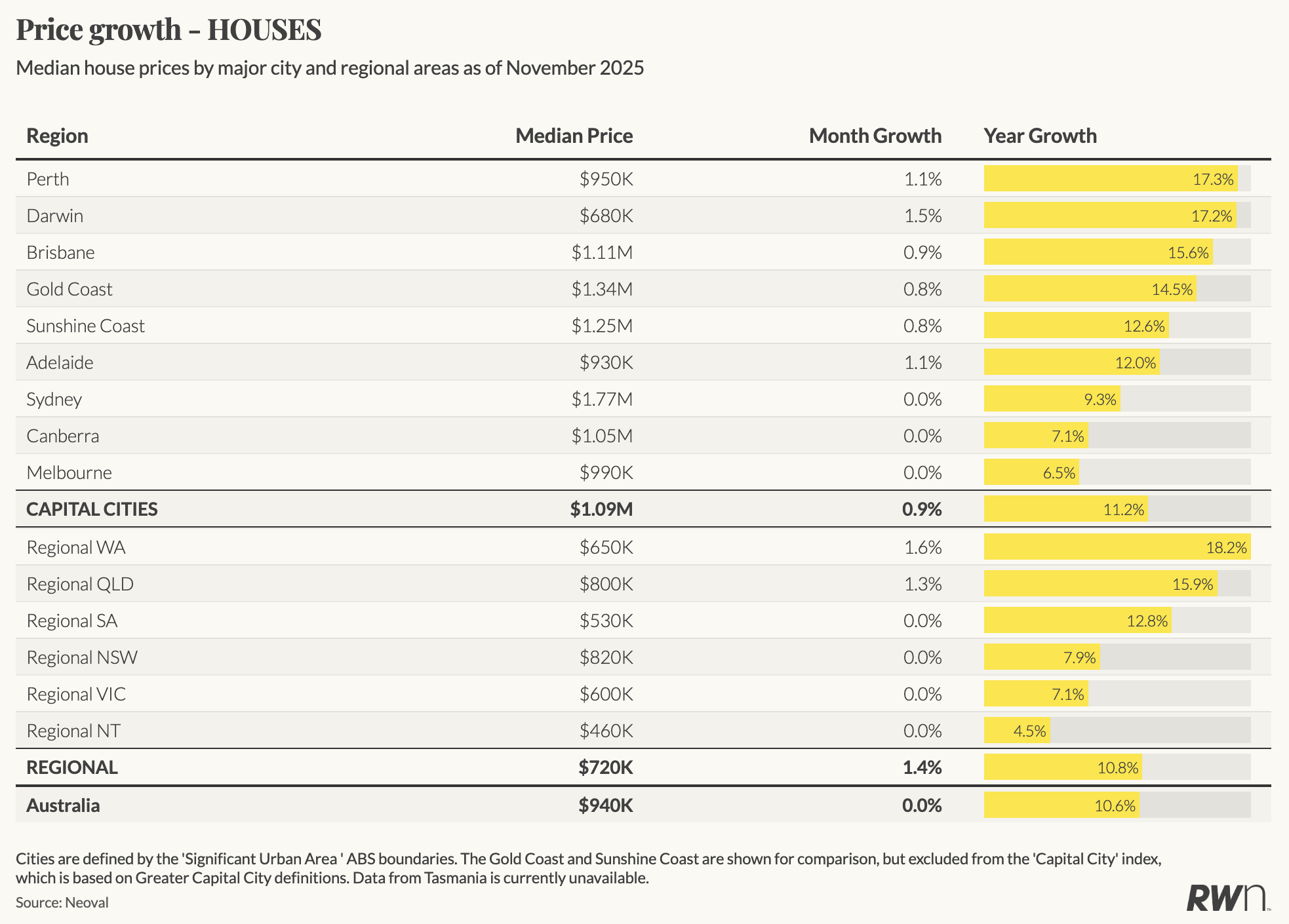

The flat national result reflects a slowdown in the larger east-coast capitals. Sydney and Canberra both recorded zero monthly growth in November, while Melbourne also paused after several months of improvement.

In contrast, growth continues in the markets that have led throughout this cycle. Perth, Adelaide and Darwin all recorded monthly gains of between 1.1 and 1.5 per cent in November for houses, and remain the key contributors to national growth. These cities continue to face significant supply shortages and ongoing demand pressures.

Regional Australia also remains a key driver of momentum. House prices outside the capitals rose 1.4 per cent over the month, compared with 0.9 per cent across the capitals. Regional Western Australia, regional South Australia and parts of regional Queensland continue to post solid results underpinned by extremely low stock levels. As noted last month, smaller capitals and regional areas are expected to remain the key outperformers into early 2026.

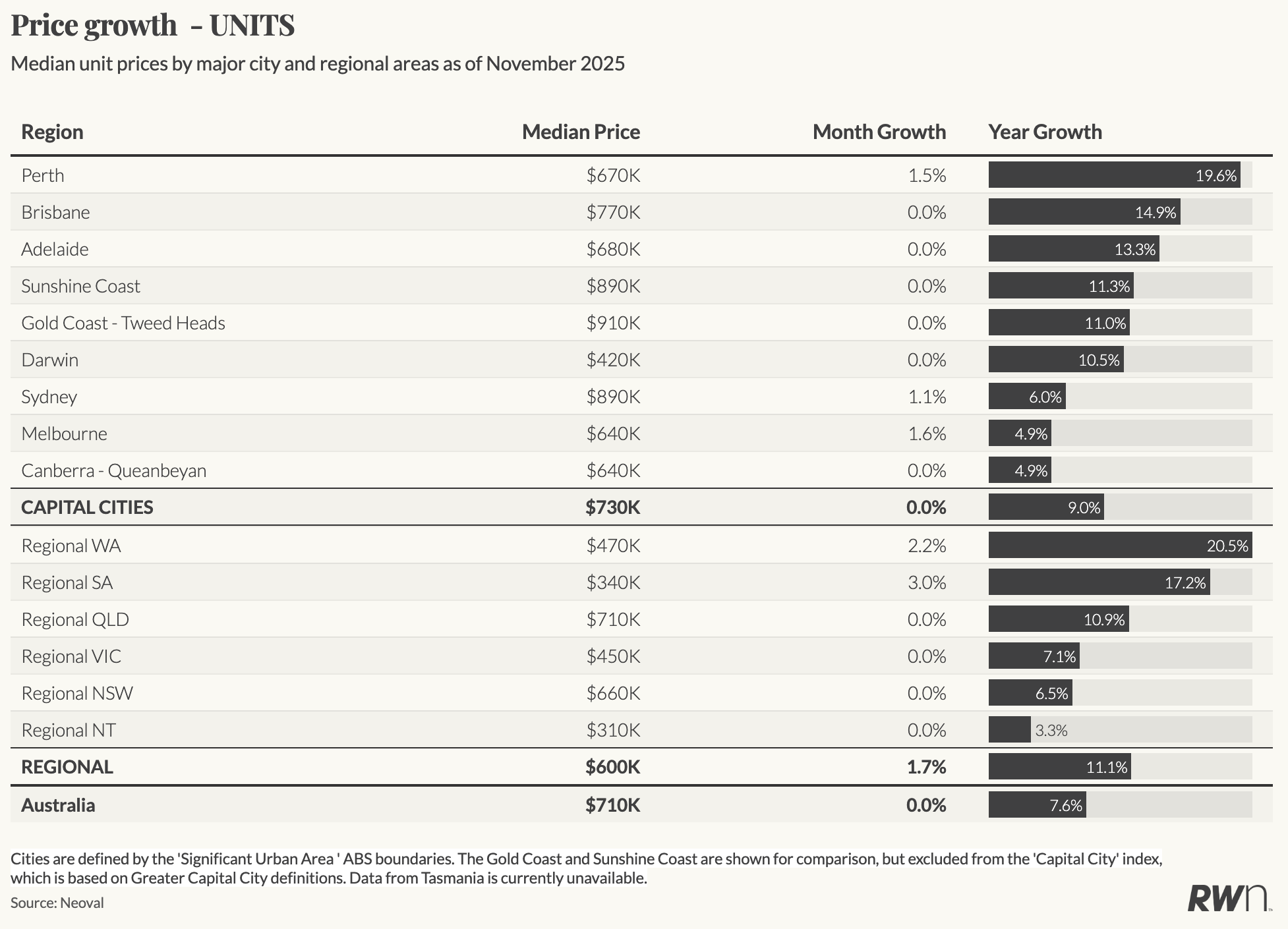

Units are showing a similar pattern. Capital-city apartment prices were flat overall, but strong monthly gains continue in Perth and several regional areas. Affordability remains a driver of demand in the unit market.

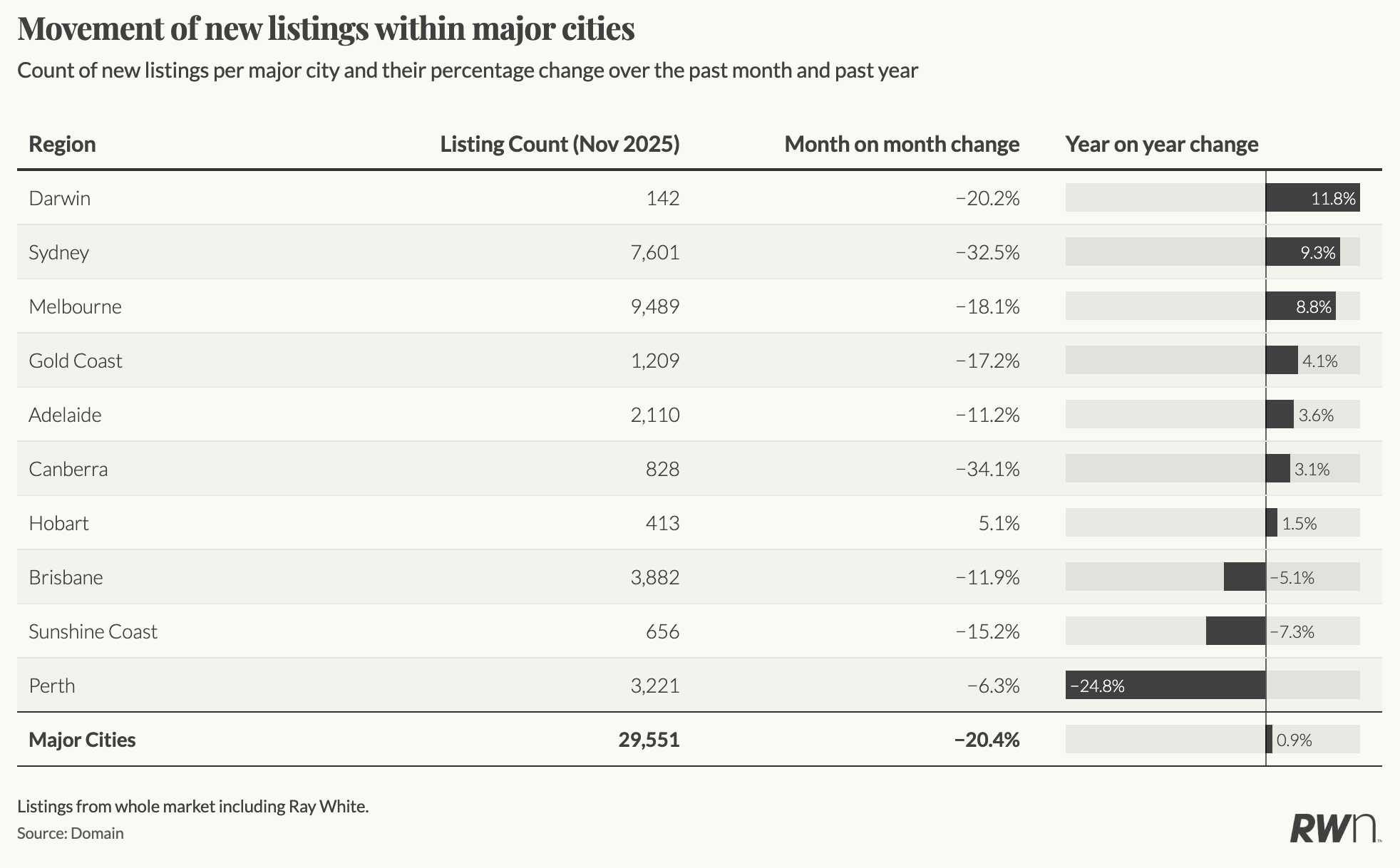

The number of properties for sale also shifted in November. After rising through spring, new listings fell 20.4 per cent month-on-month across the major capitals, with the largest drops in Canberra and Sydney. Despite this decline, newly advertised stock remains 0.9 per cent higher than a year ago, indicating that supply is still tight but broadly unchanged from late 2024. With fewer sellers coming to market, buyers are heading into summer with reduced choice.

At the same time, demand has shown early signs of easing. Average active bidders per auction declined across most major cities in November, with the sharpest fall in Perth. Brisbane, Adelaide and the Gold Coast also saw reduced bidding depth. Clearance rates remain steady, but fewer competing bidders point to more measured buyer behaviour as higher borrowing costs continue to constrain purchasing power.

This softening in auction competition aligns with a notable shift in interest rate expectations. Stronger-than-expected inflation has pushed back the anticipated timing of rate cuts, increasing the likelihood that borrowing costs will remain elevated for longer. While this could further temper demand, the simultaneous drop in new listings is likely to offset some of that moderation by limiting available supply. As such, the balance of softer competition but fewer properties coming to market suggests that price momentum may continue to ease, but widespread declines remain unlikely for now.