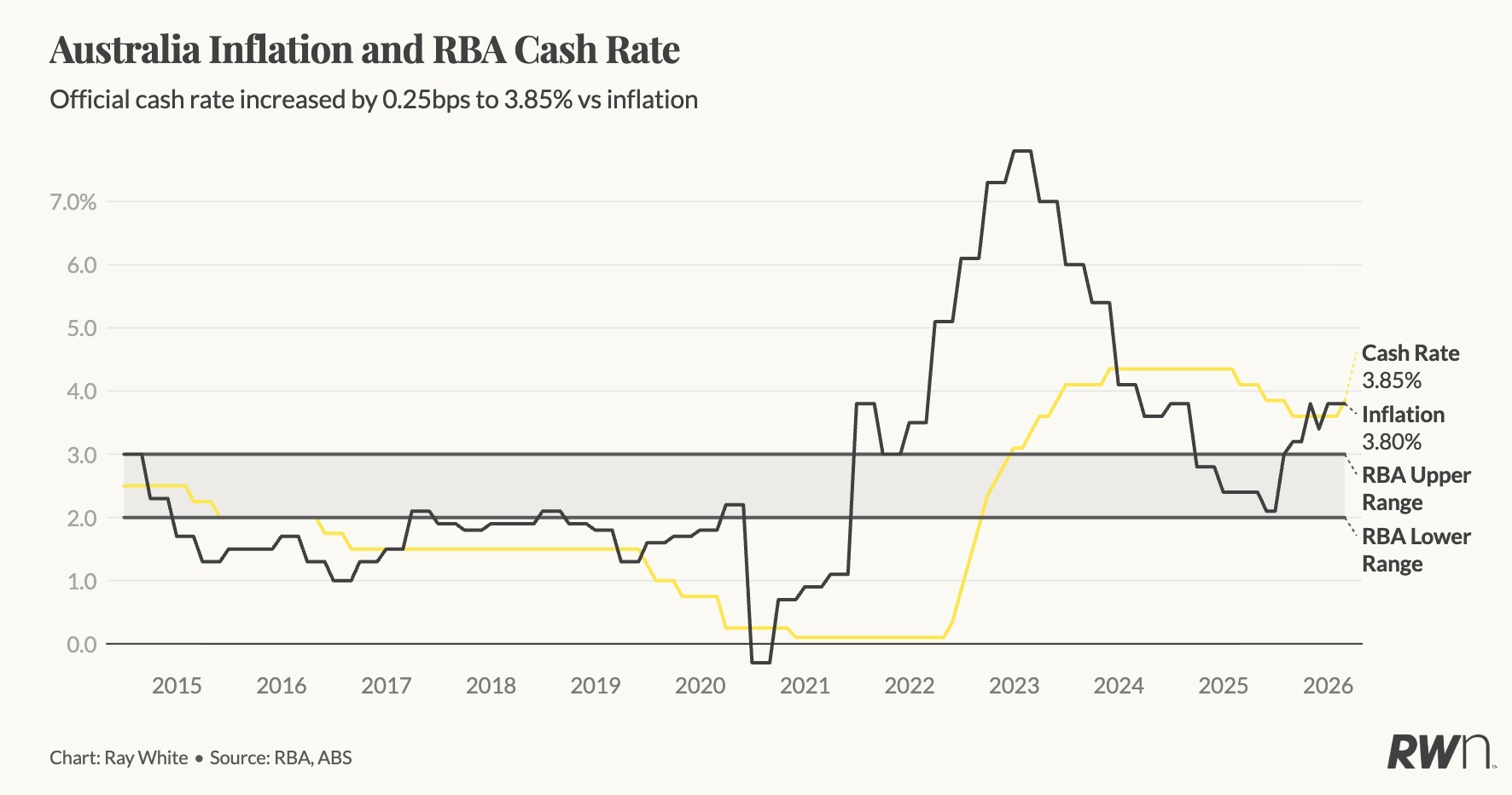

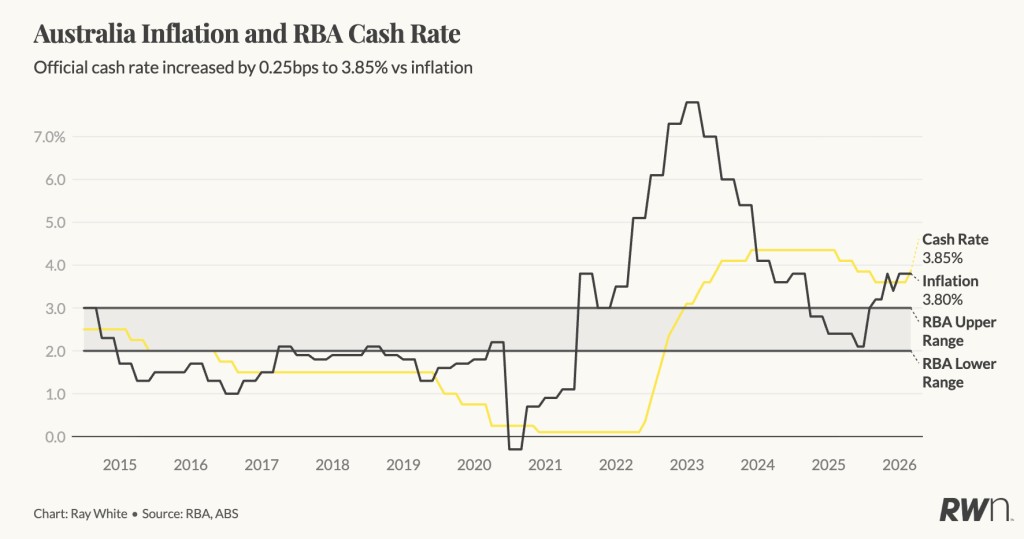

The Reserve Bank has raised the cash rate by 0.25 percentage points today, responding to inflation that remains above target and an economy that continues to run too strongly for the Bank to be confident price pressures will keep easing on their own.

Inflation surged late last year and, while it eased again in December, it remains too high. Headline CPI is 3.4 per cent and underlying trimmed mean inflation 3.2 per cent, still above the RBA’s 2 to 3 per cent target band. The recent easing has been welcome, but not sufficient for the Bank to declare that inflation is back under control.

Financial markets went into this meeting pricing roughly a 50 per cent chance of a rate increase, which reflects how finely balanced the decision was. Ultimately, the RBA has judged that the risks of allowing inflation to remain above target for too long outweigh the risks of further tightening.

The labour market continues to give the Bank room to act. Unemployment remains low at 4.1 per cent and employment is still growing, supporting household incomes and spending. With demand holding up and wage growth yet to slow materially, the RBA has chosen to lean against inflation rather than risk it becoming entrenched.

Housing presents one of the biggest policy trade-offs. Rents, electricity and new dwelling costs remain major contributors to inflation, but these pressures are being driven by a shortage of homes rather than excess demand. Higher interest rates will not fix that shortage. In fact, by increasing financing costs for developers and investors, higher rates are likely to further restrict new supply and place additional upward pressure on rents.

Australia’s housing market has remained resilient despite high interest rates. Prices rose about 12 per cent in 2025, driven by strong demand and very limited supply. Higher rates will slow price growth in 2026 by constraining borrowing capacity and buyer activity, but they are unlikely to reverse the underlying shortage of homes that continues to support prices.

Today’s decision signals that the RBA is not yet satisfied that inflation is on a secure path back to target. With the economy and labour market still strong, the Bank has chosen to apply further restraint to ensure inflation is brought back under control.