Nerida Conisbee

Ray White Group

Chief Economist

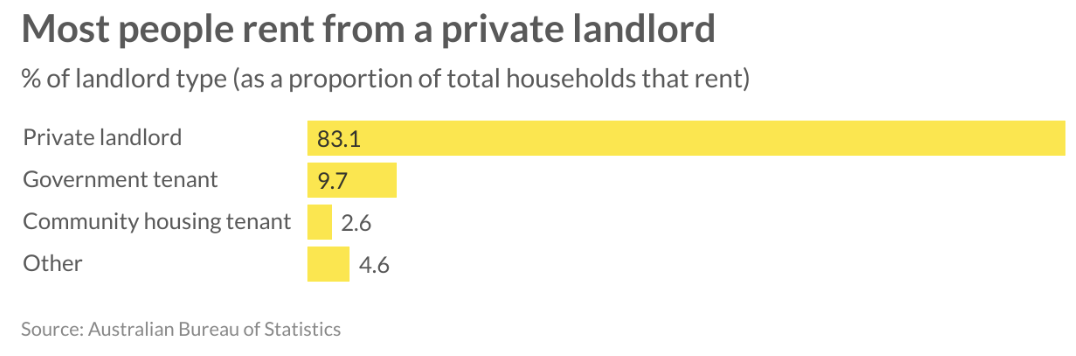

Private investors (“mum and dad” investors) provide most rental properties in Australia. If tax policy is changed that makes owning a rental property less attractive, there will immediately be far fewer rental properties available. Right now there is no group that can step in quickly to address this shortfall. The negative gearing debate needs to be considered with this in mind, particularly now that there are too few rental properties and will be for quite some time.

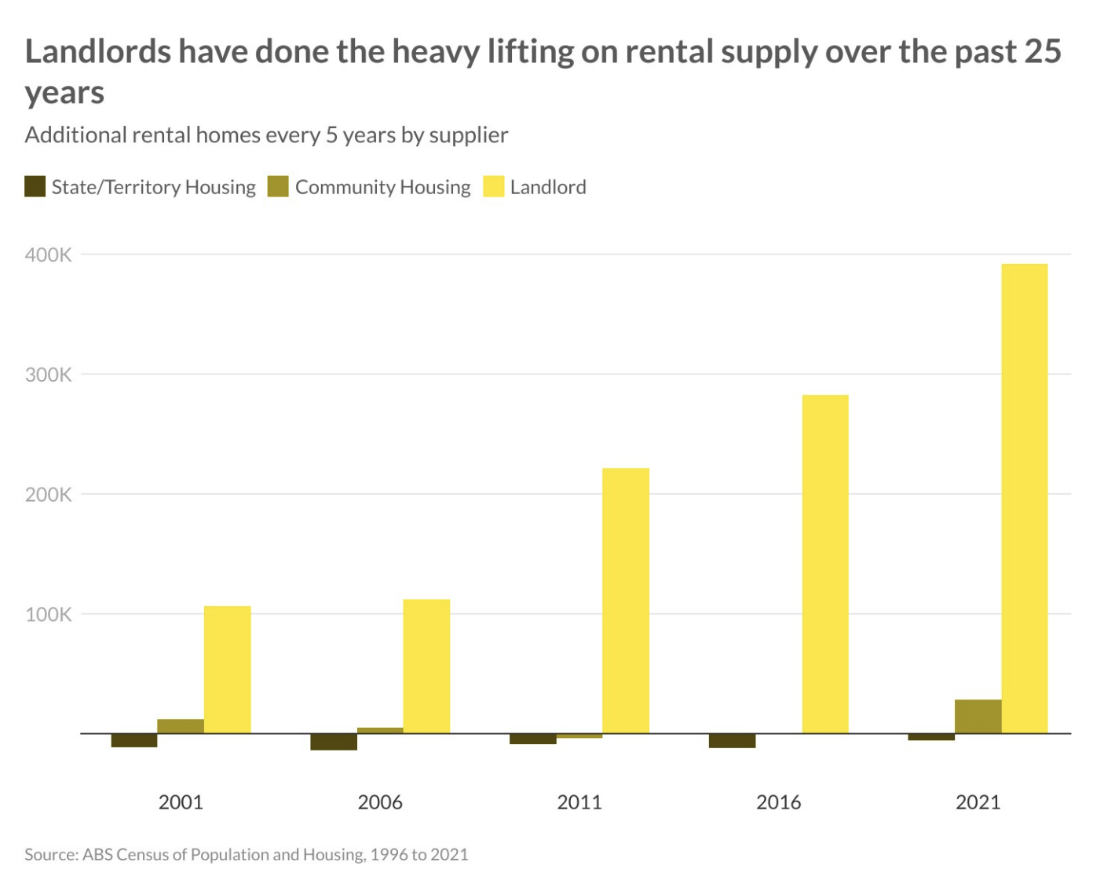

Although they are frequently criticised, incentives available to property investors in Australia have been successful in providing a steady stream of rental properties and keeping the proportion of households under rental stress at globally low levels. Between 1996 and 2021, there were an additional 1.1 million rental properties provided by investors.

Compare this to an increase of 41,000 homes provided by community groups and a loss of 53,000 rental properties provided by the government.

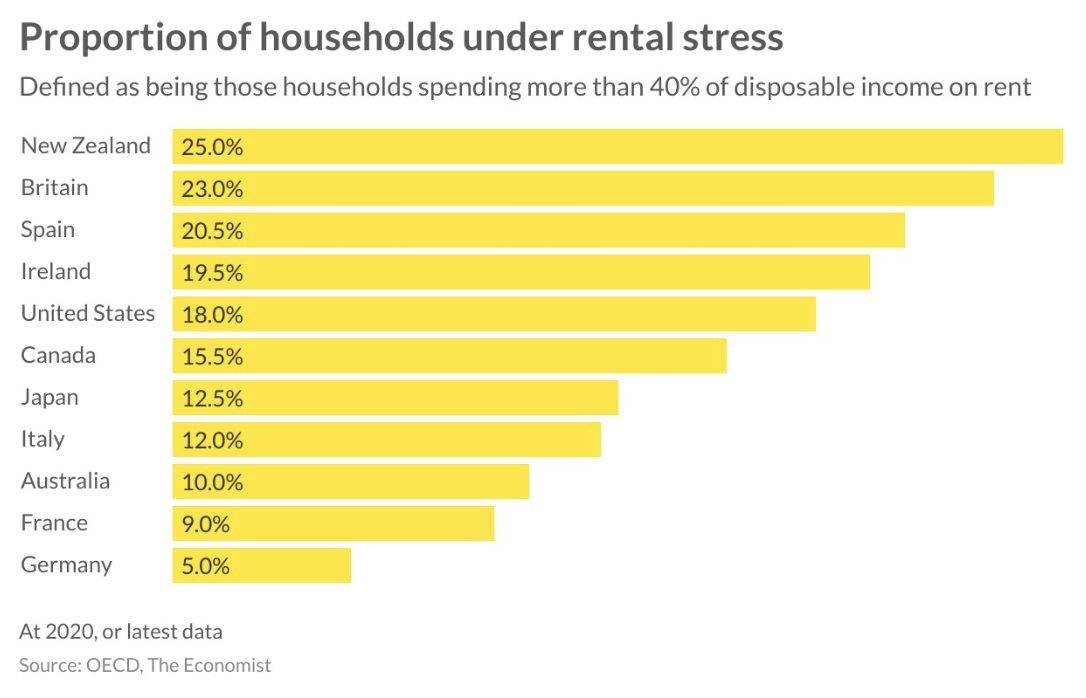

Rental stress has been kept low at a global level. An analysis of OECD data has shown that the proportion of households under rental stress is relatively low at 10 per cent. As a comparison, New Zealand, Britain and Spain all have very high levels of stress, exceeding 20 per cent. While this measure would have increased since the start of the pandemic, the rental shortage is similar everywhere around the world and other countries would have seen similar increases.

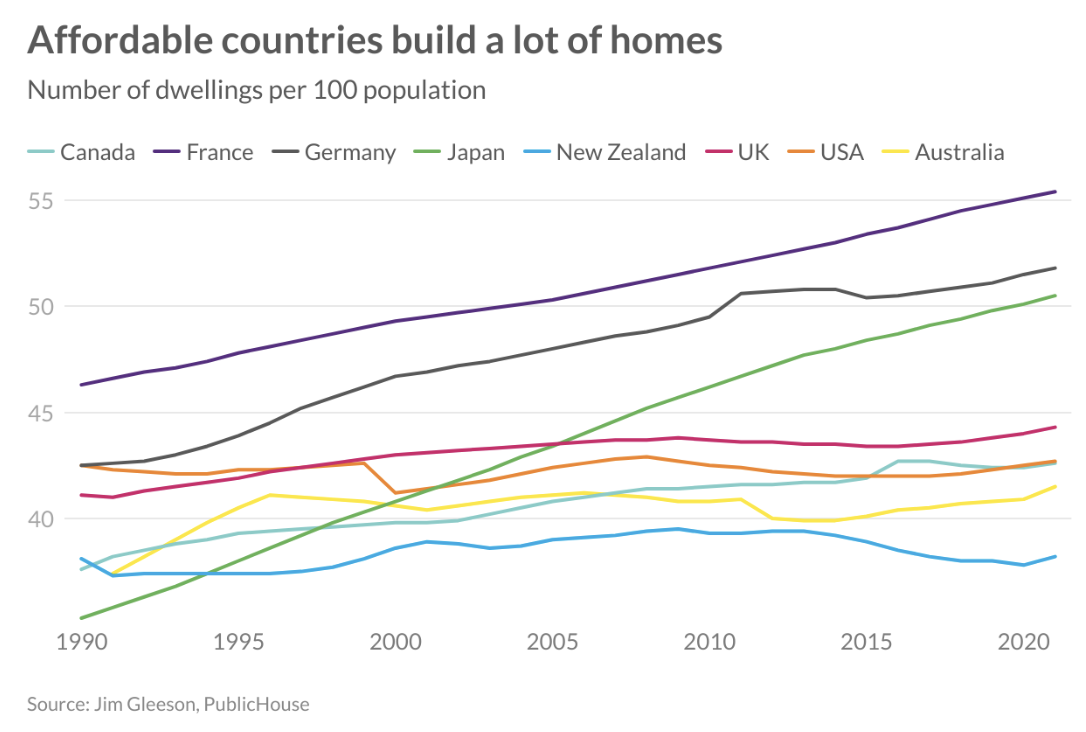

What is even more interesting however is that Australia has maintained this low proportion of rental stress even though we have not built enough new homes relative to our population growth.

France and Germany have maintained rental affordability because they build a lot of homes relative to population growth. New Zealand has built the least which explains their lack of affordability. Australia has also under built over a long time but has maintained higher rental affordability. It is likely that negative gearing has been a major contributor to this.

Many investors rely on negative gearing to make the investment viable and a loss of this incentive will lead to a large number selling. This will reduce the number of rental properties immediately. There are groups that could potentially step in but they are not ready to provide the amount required. In some cases, they are not interested or lack the capability to provide scale.

Historically, State/Territory Governments have supplied rental housing, however this has been reducing steadily over the last 20 years. Theoretically, this could be reversed, although many of the problems that face private developers would also face the government sector.

Construction cost rises have made building new homes more expensive to build. A push back from local residents can make adjusting planning controls difficult, particularly in inner and middle ring suburbs. A development and management arm of the government would need to be set up to get enough homes built, not something that can be done quickly

The difficulties for governments in trying to reverse the steady decline in their rental housing stock was most recently evidenced in New Zealand. With growing rental problems, Kiwibuild was introduced in 2018 to provide 100,000 affordable by 2028. The program was originally run by the Ministry of Business, Innovation and Employment as an interim measure until a new Housing Commission could be established. By 2021, the scheme had only produced 1,000 homes and the target was given up. The scheme is still in play but the future is now uncertain given its lack of success.

Build to rent, or institutional owners, of rental properties are another group that could provide housing but similarly to government, can’t move quickly enough to replace a rapid drop in rental properties. At present, build to rent provides less than two per cent of total rental housing. The number of developers building these projects is small and their ability to scale up quickly is limited. In addition, the types of homes that Australian build to rent developers are focusing on at present are apartments which are not suitable or desirable for all renters.

It is also naive to think developers of build to rent won’t require a good return and if the return is not great, will also need to be subsidised through tax incentives or by charging higher rents. While private investors will buy a rental property that provides a sub three per cent yield, build to rent developers and owners will require a much higher yield. This is because they typically can’t rely on the possibility of future capital growth to justify a development.

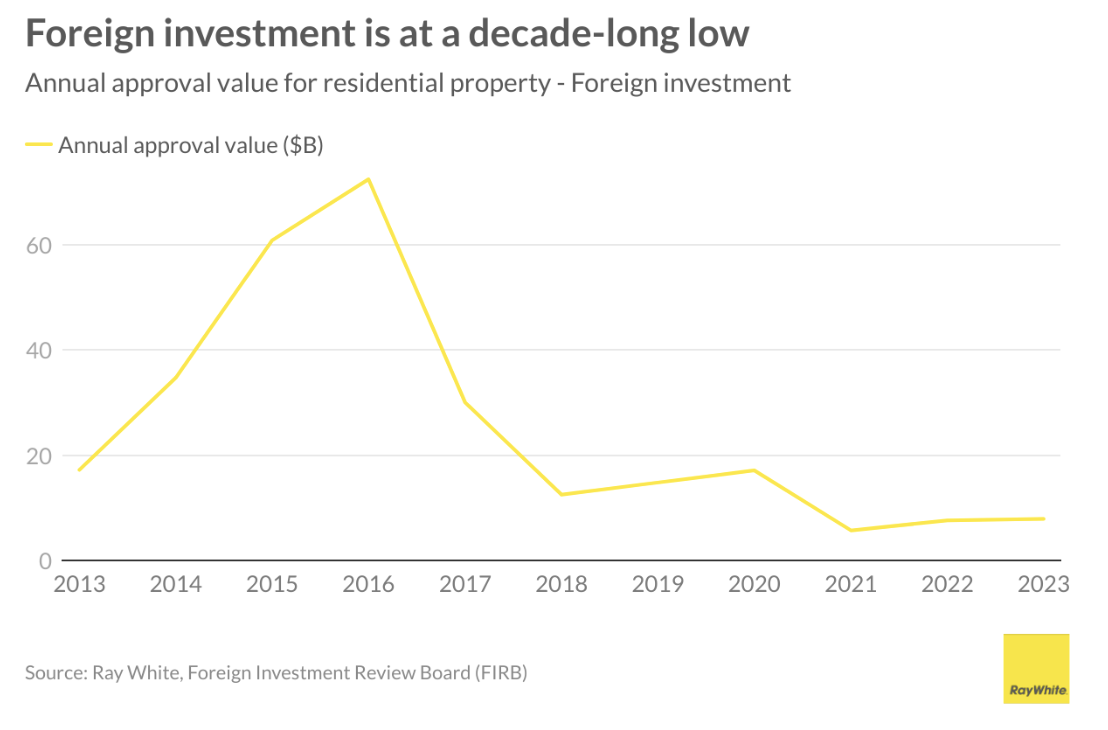

Foreign investors have been significant suppliers of rental properties in Australia, however won’t return in the same way as last decade. Even if many of the additional taxes we placed on foreign investors last decade were clawed back, restrictions imposed by foreign governments, particularly Chinese, make it difficult to invest in Australia.

Taxation systems should be reviewed regularly but the process needs to be done slowly and carefully and this is particularly the case for negative gearing. We have relied on it for a long time to ensure enough rental properties and for the most part it has worked. More immediately, we need to focus on building enough homes.

Similarly, a push to move to a land tax system to prevent homes being under utilised or simply left vacant should be encouraged. A sharper focus should also be made on providing affordable homes to those that really need it.